Good morning!

This week the OCC rewrote the rules on model risk management for the first time since 2011, and flagged that AI-specific rules are coming next. Same week, bank M&A hit a seven-year high.

Those two things are connected. The banks building AI into their operations now are the ones with the leverage to stay independent.

TRENDING AI NEWS FOR CB

OCC just rewrote model risk guidance, and an AI-specific rulemaking is next.

On April 17, the OCC, Federal Reserve, and FDIC replaced the 2011 model risk framework. New rules are risk-based and scaled by size, primarily aimed at banks over $30 billion. Generative and agentic AI are out of scope. What matters for your bank is what comes next: a separate AI-specific RFI is confirmed and coming soon.

Why it matters for your bank: That RFI will shape how your examiner thinks about generative AI. Get your governance in order before it lands.

OpenAI now has a dedicated finance team inside ChatGPT. The race is on.

On April 13, OpenAI acquired Hiro Finance, its second personal finance startup in a year. The product shut down immediately. The entire team moved inside ChatGPT to build AI-powered financial guidance at scale. A TD Bank survey found 55% of Americans used AI for financial decisions this year, up from just 10% last year.

Why it matters for your bank: That five-fold jump happened before OpenAI had a dedicated finance team. Community banks win on relationships, and that relationship starts with financial guidance. Banks that build that experience into their own digital products keep the conversation. Banks that wait will find the habit is already formed somewhere else.

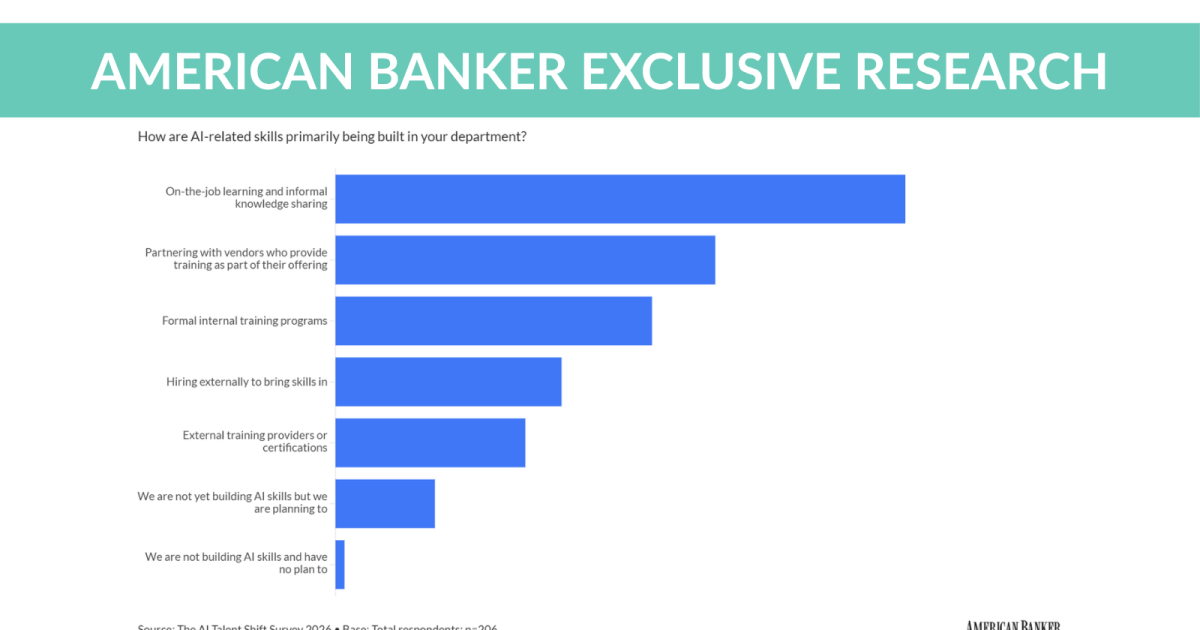

AI fluency is up at community banks. Strategy still isn't.

American Banker's 2026 AI Talent Shift Survey found 61% of community bankers now report moderate to high AI fluency, built mostly through informal, on-the-job learning. Only 32% said AI is a top strategic priority at their institution.

Why it matters for your bank: Fluency without strategy produces expensive pilots that never reach production. The banks pulling ahead picked two or three high-impact workflows, went deep, and measured results.

DEEP DIVE

Two banks. Same market. One gets acquired. Why?

Bank M&A is at a seven-year high. Deal volume is on track to double in 2025. The buyers are not just chasing deposits; technology costs, compliance infrastructure, and AI investment have become fixed costs that do not scale down for a $500 million bank the way they do for a $5 billion one.

Banks under $1 billion are facing a shrinking buyer universe at the very moment more are considering selling, because the midsize banks that historically acquired them are themselves being acquired.

The banks not in that conversation have leaner cost structures because they automated the workflows that eat time. Per-loan production costs have averaged over $11,000 in recent quarters, well above the long-run average of $7,800, and personnel is consistently the largest component. That is the number that determines whether a $700 million bank survives independently or gets absorbed.

AI does not save community banking by making it more digital. It saves it by making the relationship banker's time worth more.

Three things to do this week:

Ask your lending team how many hours are spent on document collection and status chasing. That is your business case for AI document automation.

Look at your per-loan origination cost trend. If it has climbed over the last three years, manual processing is almost certainly the driver.

Take the consolidation conversation to your board as a planning frame, not a threat. Banks that reduce their cost structure now have the most options later.

Consolidation Analysis — Banking Dive

FROM MULTIMODAL

🇸🇬 We're on stage in Singapore next week

Multimodal was selected by Singapore's Ministry of Home Affairs for Hatch DimensionX, a government accelerator. Our proof-of-concept with the Singapore Police Force goes live on stage at Milipol TechX on April 29. If you are attending, come find me.

Can't make it to Singapore? See the same product working for your banks

Data point this week

43

FDIC-insured banks disappeared in Q4 2025 alone. 36 through mergers. That pace has not slowed. The question is whether your cost structure is ready.

Source: FDIC Quarterly Banking Profile, Q4

ONE QUESTION FOR YOU

What is the one workflow at your bank that costs the most time and produces the least relationship value?

Hit reply.